Buy Side Sentiment Tracker

February 2026

Views from 44 top asset managers across 73 assets, based on 1,300+ individual views

We have moved!

Sentiment Matters is the new home of my work on Investor Sentiment & Positioning, the mood of the market, mapped and decoded.

Sign up for free or upgrade for full access at

Main takeaways

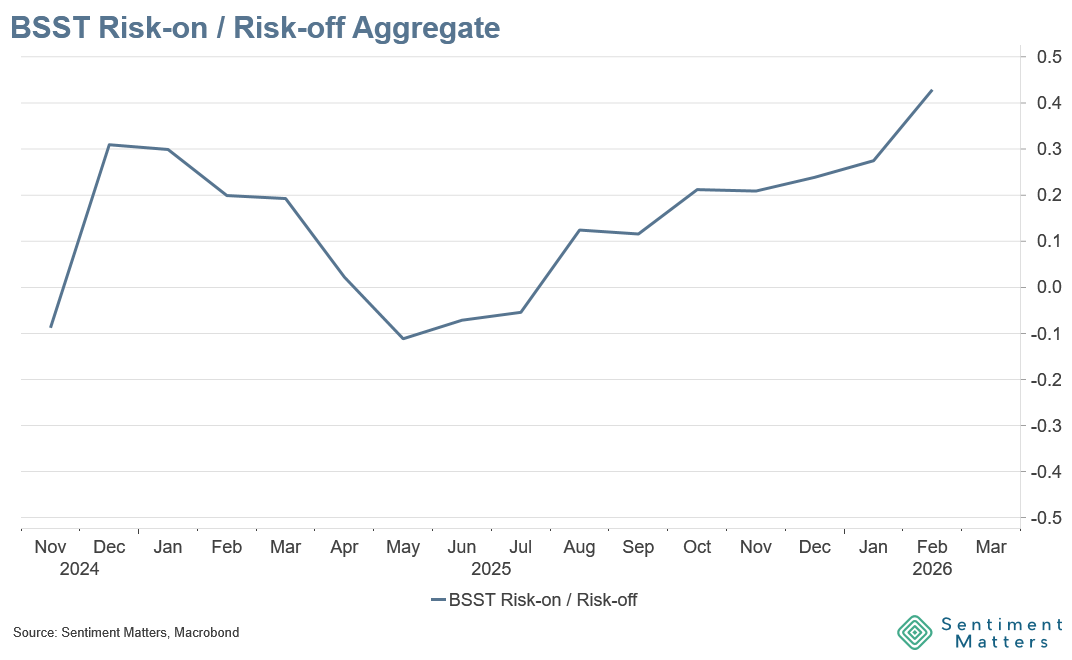

Overall sentiment: the most bullish reading since we launched the BSST in 2024 (new high, above Dec-2024)

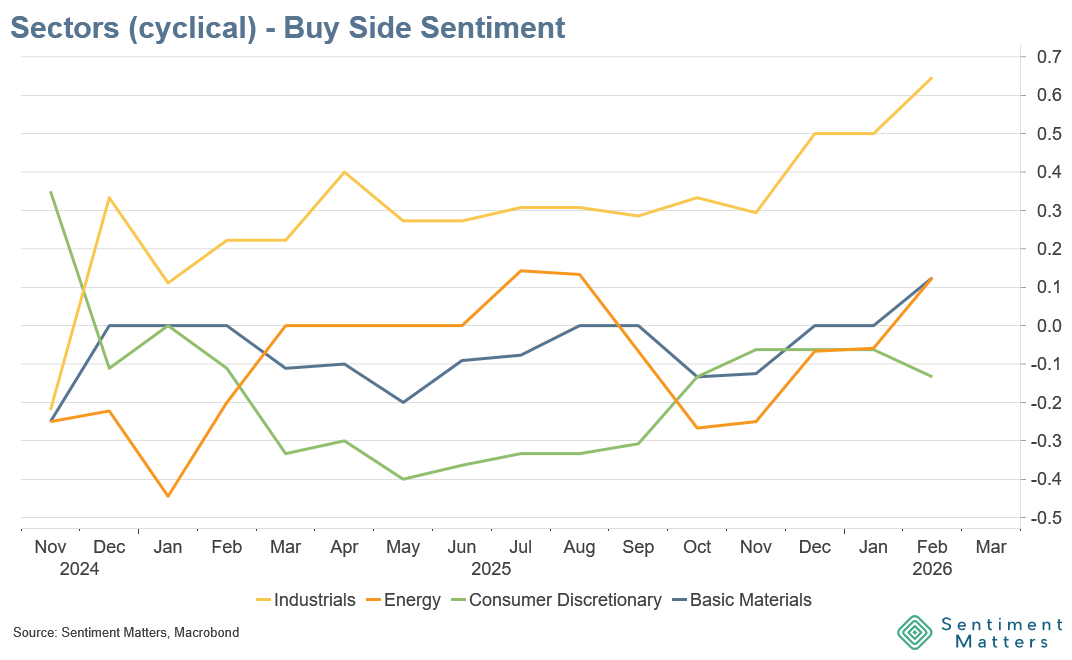

Cyclicals: the clearest message across assets is “Buy Cyclicals” (sectors + factors)

Emerging Markets: divergence is widening — EM equities & EM debt loved, while China equities downgraded for a 4th straight month

Tech: loses its #1 spot (or is barely clinging on), but remains far from unpopular

Sentiment: Record Bullishness

Buy-side sentiment took another step higher — to a new BSST high, exceeding the December 2024 peak.

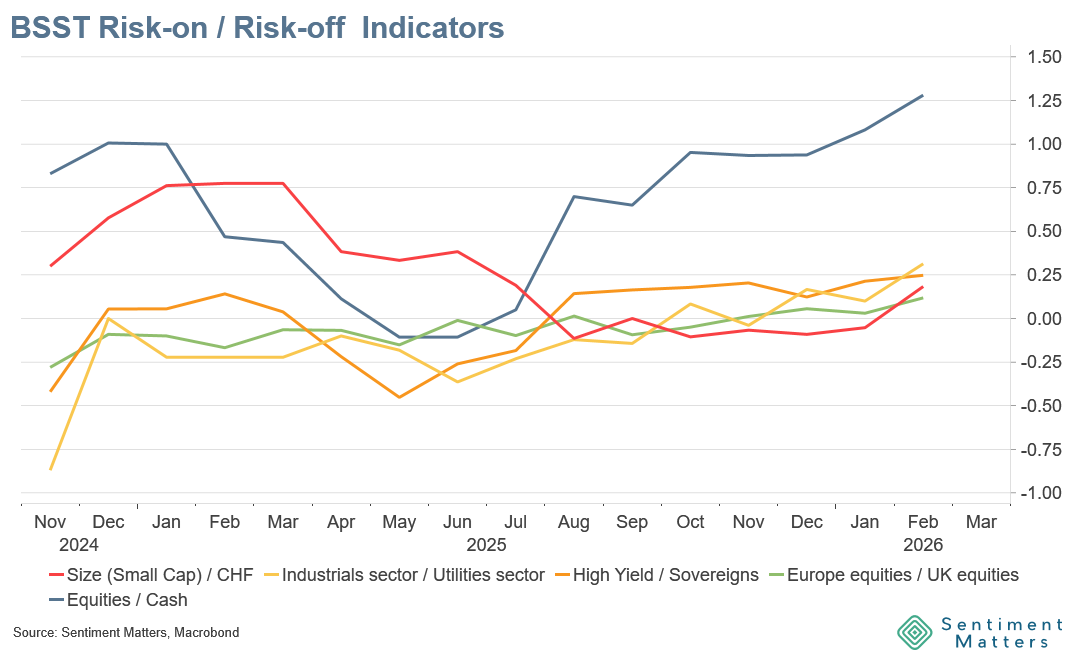

Risk appetite

Risk appetite rose in all 5 risk-on/risk-off indicators

All 5 indicators are at the highest level in the 16-month history

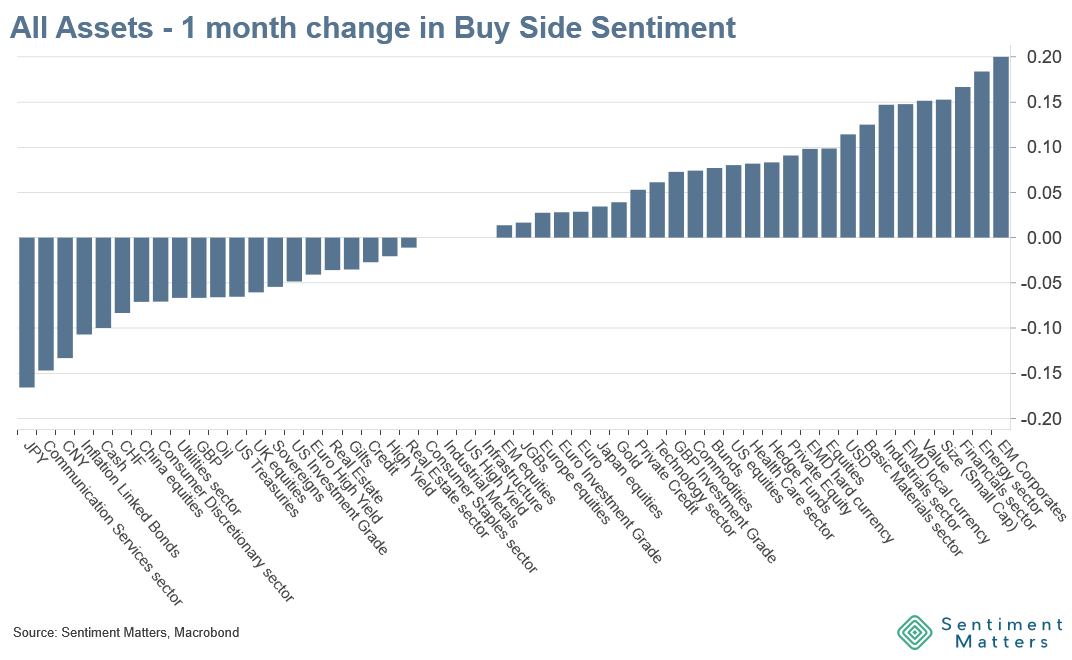

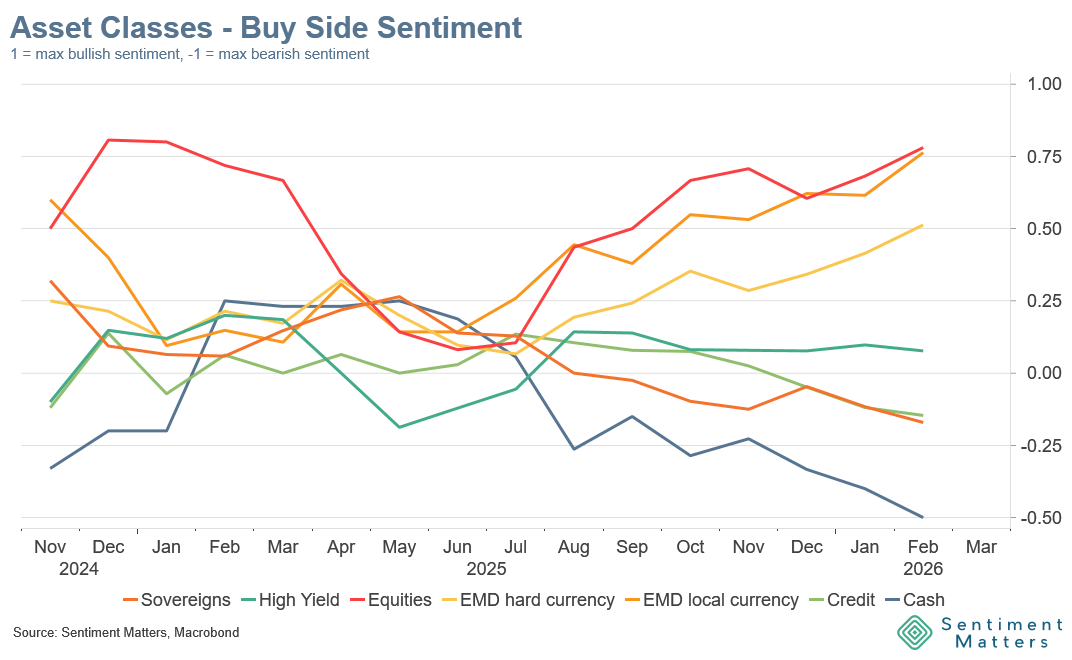

Big asset-class shifts

This was a classic risk-on month: the riskiest assets upgraded — and defensiveness (cash/sovereigns) faded further.

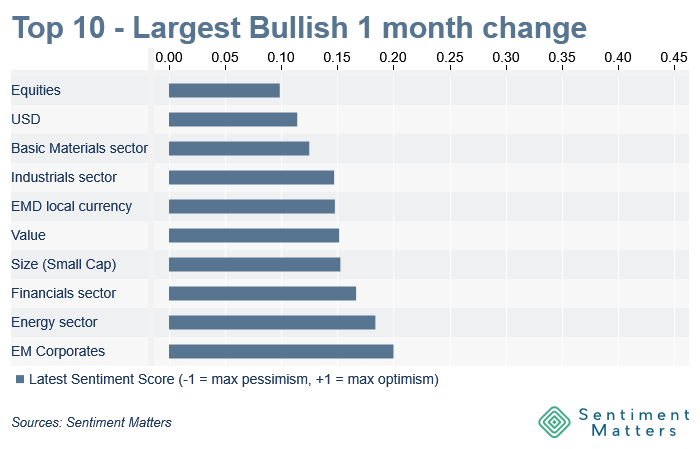

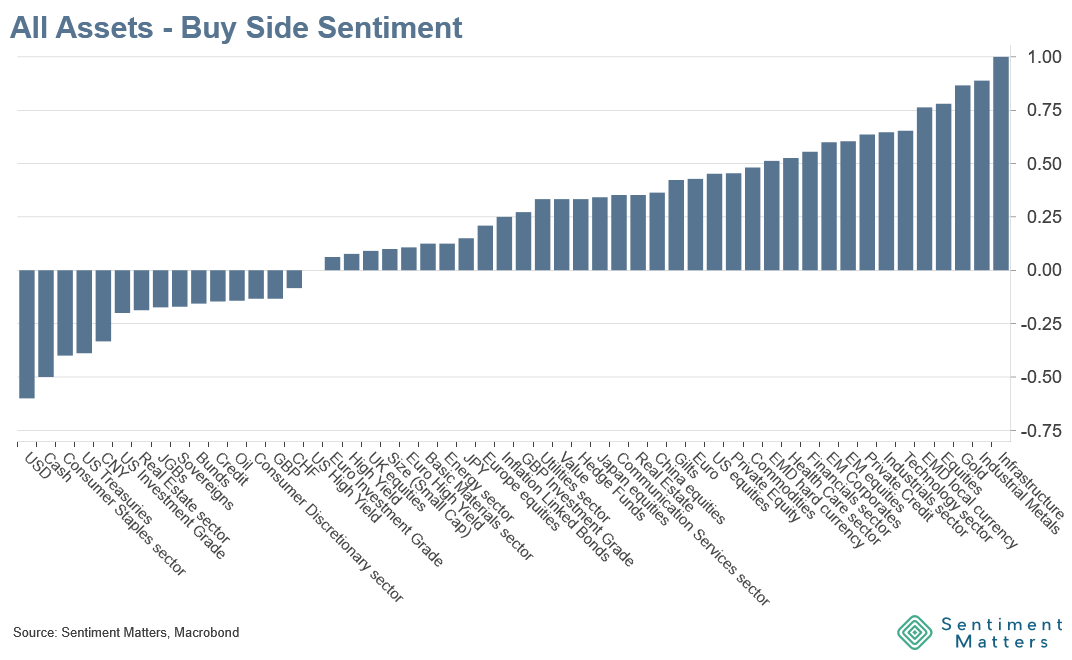

Equities: upgraded again to +78% net bullish (top major asset class)

33 Bulls | 7 Neutrals | 1 Bear

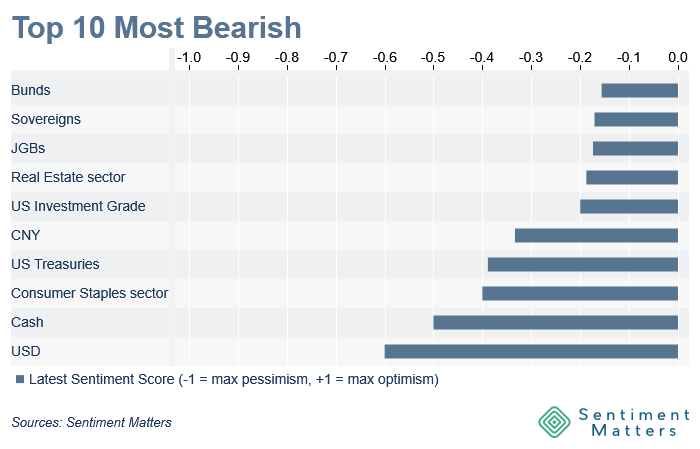

Cash: downgraded again to -50% net bearish (new low; least popular asset class by far)

Sovereigns: downgraded to -17% net bearish (2nd-lowest on record)

Positioning tilt

Clear pro-cyclical lean: biggest overweight of cyclical sectors in BSST history

Small caps upgraded to their most bullish reading in 10 months

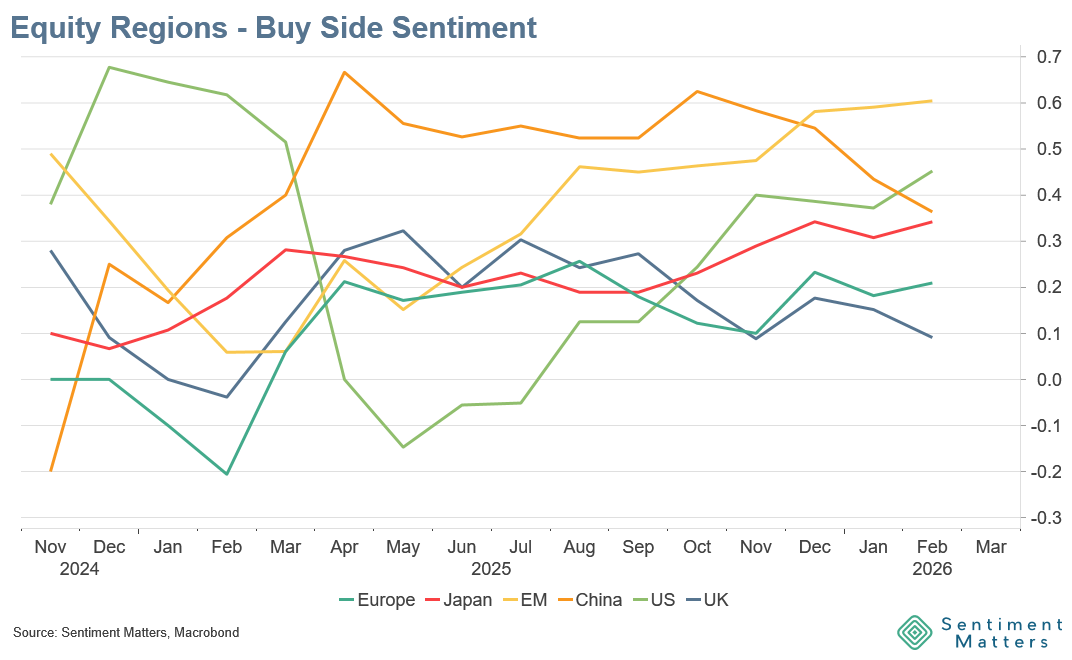

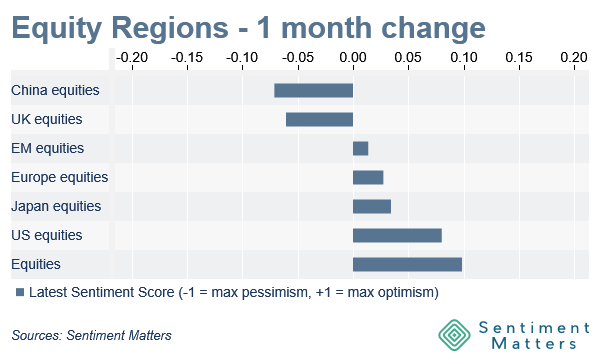

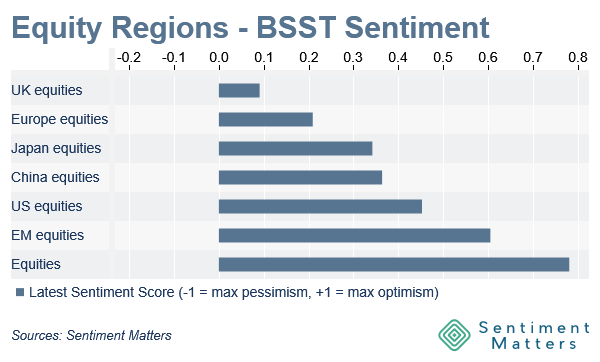

Equity Regions

US equities

Biggest upgrades among regions: a sharp recovery from “least popular” after Liberation Day to 2nd most popular.

Now +45% net bullish.

EM vs China: divergence widening

China: 4th straight month of downgrades → least bullish in a year

Rest of EM: upgraded again → +61% net bullish (top region)

New: India

First month in the tracker: 7 views → 4 Bulls | 3 Neutrals | 0 Bears

Japan

The “Takaichi bounce” is still alive: upgraded to +34% net bullish.

Most bullish in BSST history, but still room for upside if reform/fiscal optimism is confirmed by data.

Europe & UK

Europe: small upgrade, but sentiment has treaded water since last spring — still net bullish, but 2nd-least popular region.

UK: least popular region for a 4th month — not surprising in a month where investors are pushing pro-cyclical exposure.

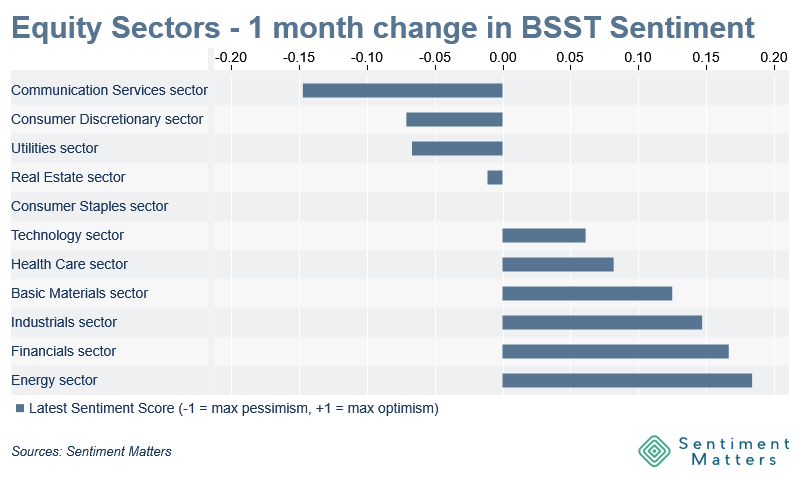

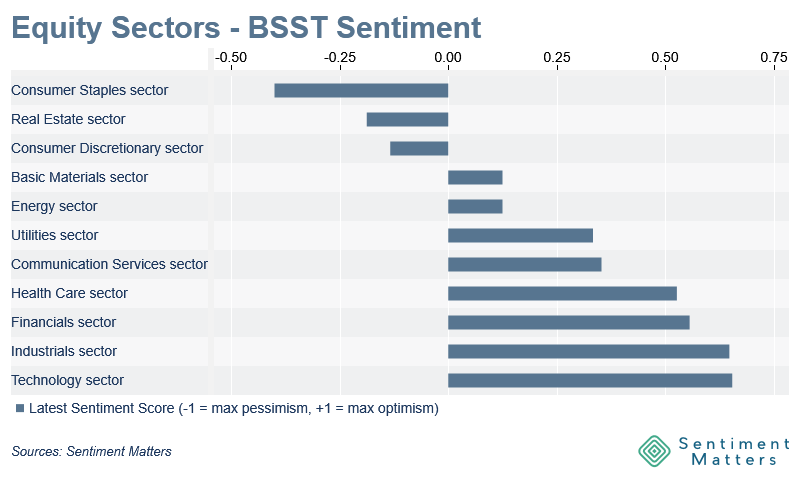

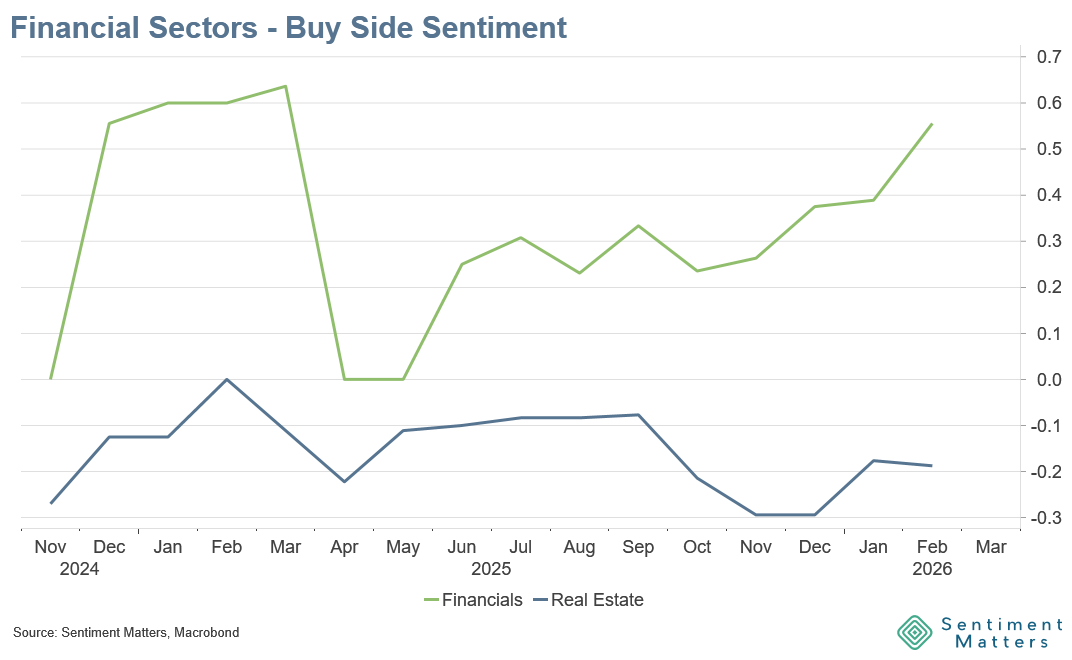

Equity Sectors

Cyclicals led the upgrades

Broad upgrades across Energy, Industrials, Materials

Financials also benefited (cyclical characteristics)

This was the clearest pattern across sectors.

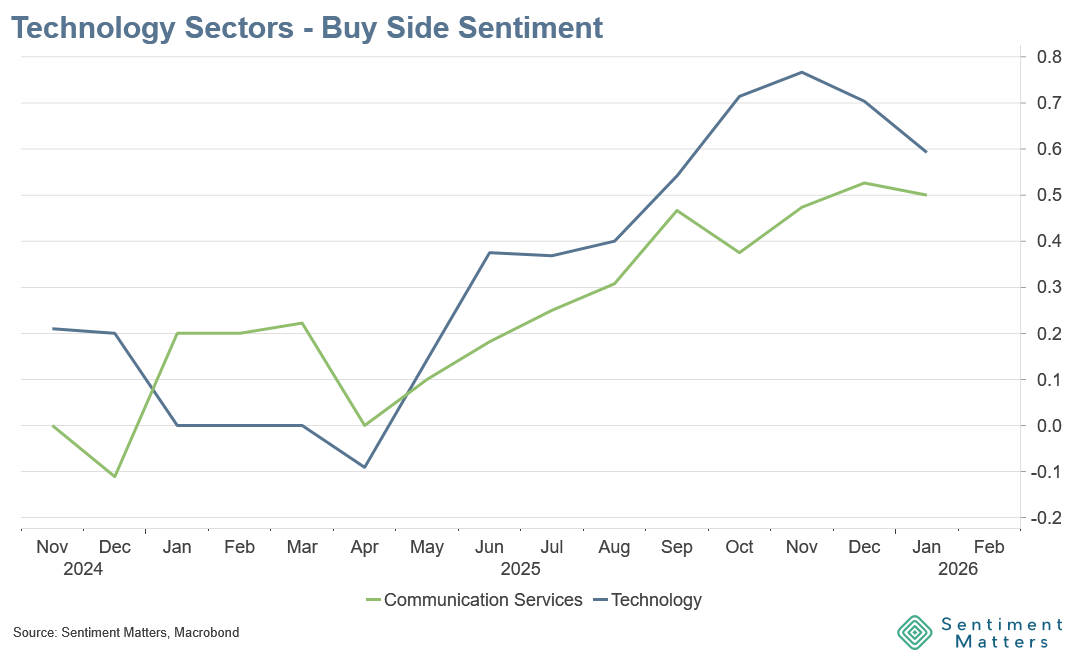

Tech: cooling, not capitulation

Technology: still at/near the top, but no longer running away with it.

Importantly: Tech underperformance has not triggered meaningful capitulation-style downgrades — consistent with what other sentiment indicators show.

Where the downgrades were

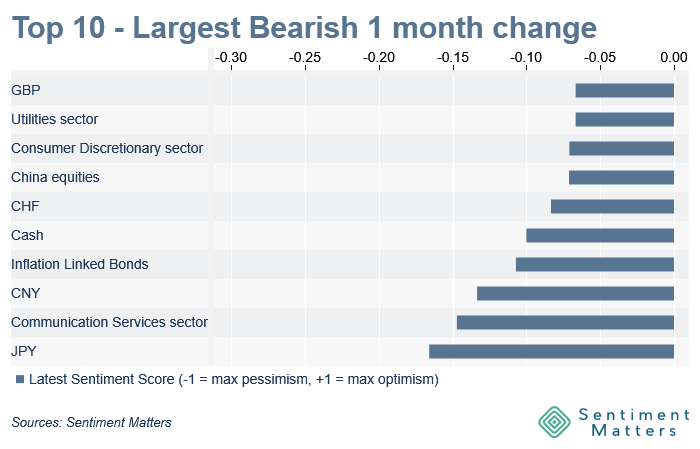

Communication Services: largest downgrades (another tech-heavy pocket) —consistent with broader sector sentiment.

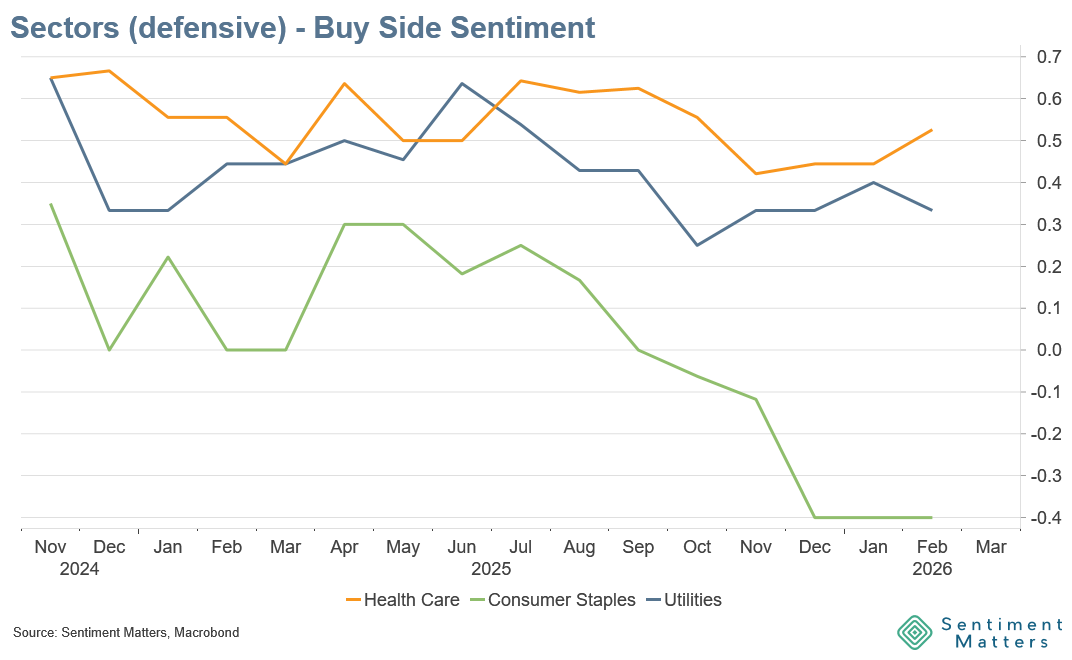

Defensives

Mixed, but the broader story was cyclicals up rather than defensives down.

Health Care and Utilities remain net popular.

Consumer Staples

No fresh downgrades this month, but still -40% net bearish — weakest sector and close to historical extreme pessimism territory.

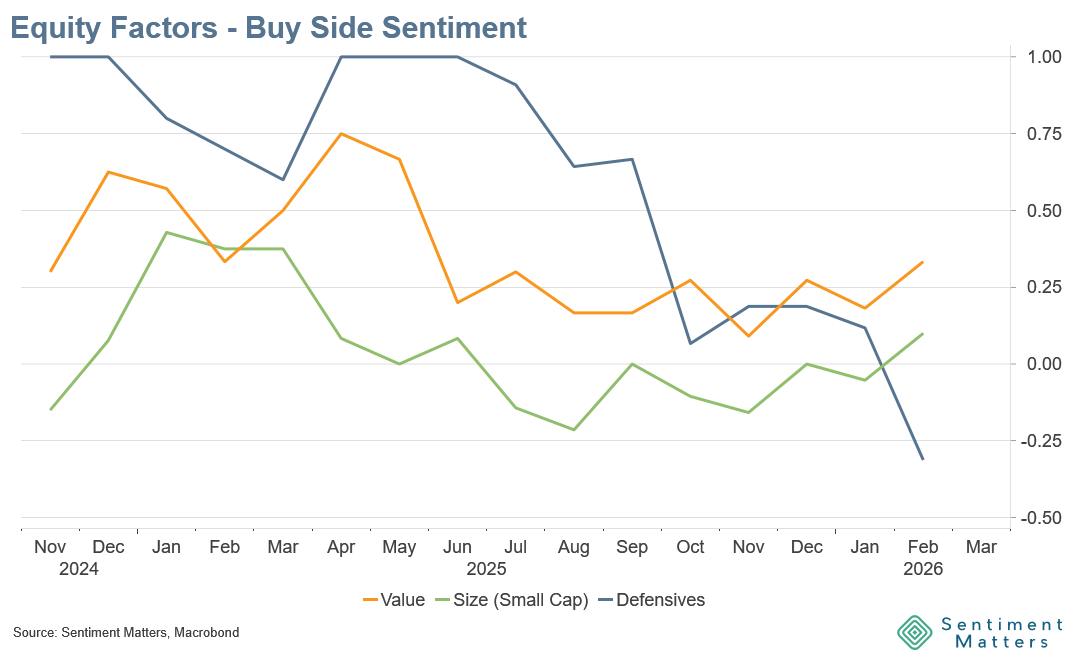

Equity Factors: Value > Size

Value and Size both upgraded, but remain well below their popularity a year ago.

Value remains the most popular factor at +34% net bullish (still well within the past year’s range).

EU factor reads (small samples)

EU Value: scarce views (3 total); 2 of 3 bullish

EU Small Caps: more coverage and more positive: 5 views, all bullish

Small caps

Upgraded in line with the pro-cyclical shift.

US small caps now most popular since last April, though sentiment is still only +10% net bullish — plenty of upside potential if the rotation continues.

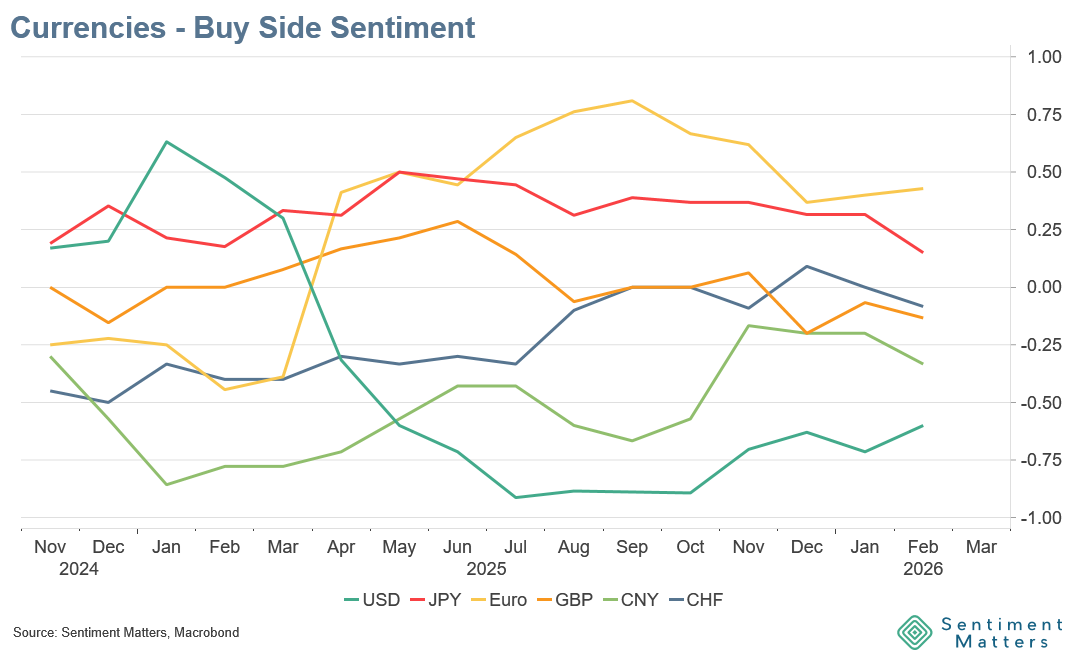

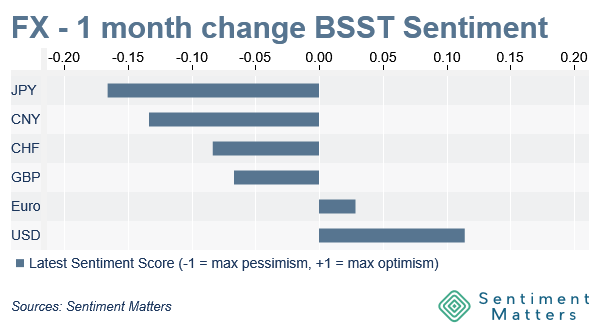

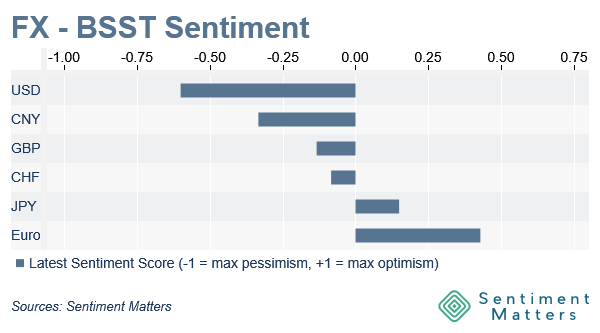

Currencies

US dollar: third upgrade in four months, but still the most bearish asset in the entire 73-asset universe.

This time last year: +62% net bullish → today: -60% net bearish (largest 1-year reversal by far)

GBP: downgraded; slightly net bearish, mid-pack.

EUR & JPY: remain the preferred G10 counterparts to a USD short

EUR: less bullish than summer, but still by far the #1 currency long

JPY: biggest downgrade of any asset this month — from very popular in May to roughly neutral now

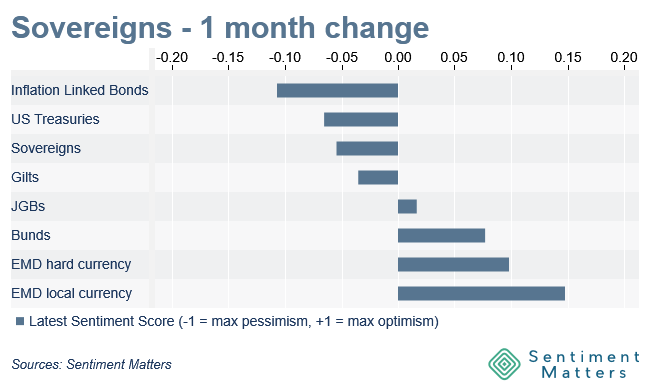

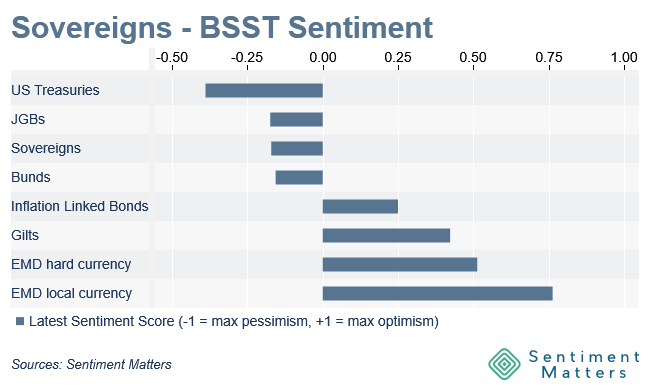

Sovereigns

Despite the asset-class downgrade, the picture underneath is mixed.

Two clear buckets

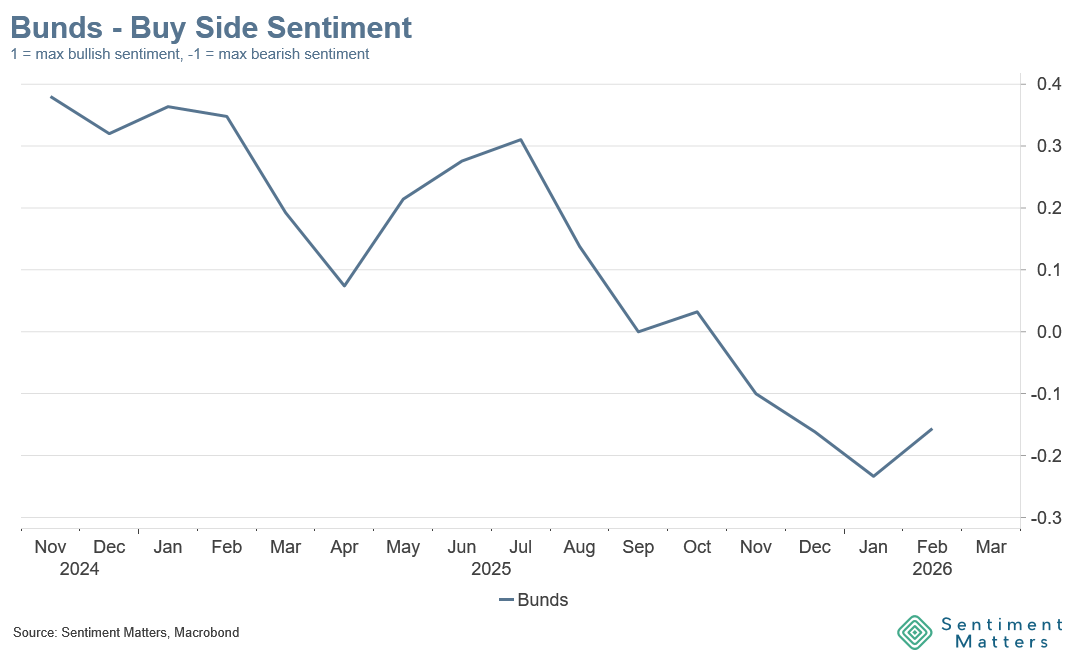

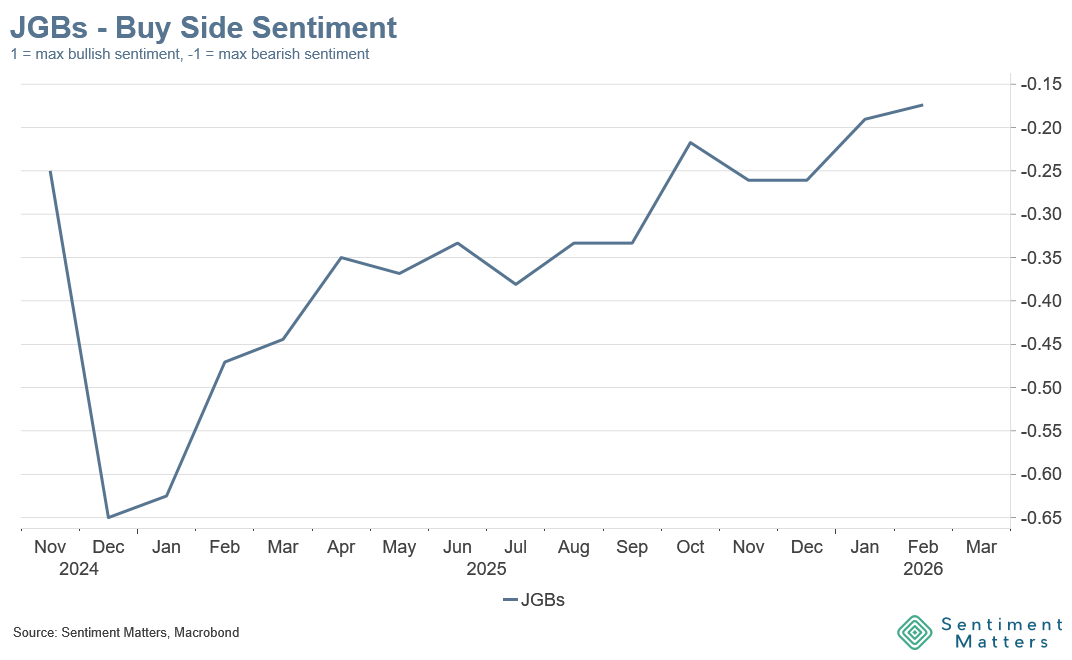

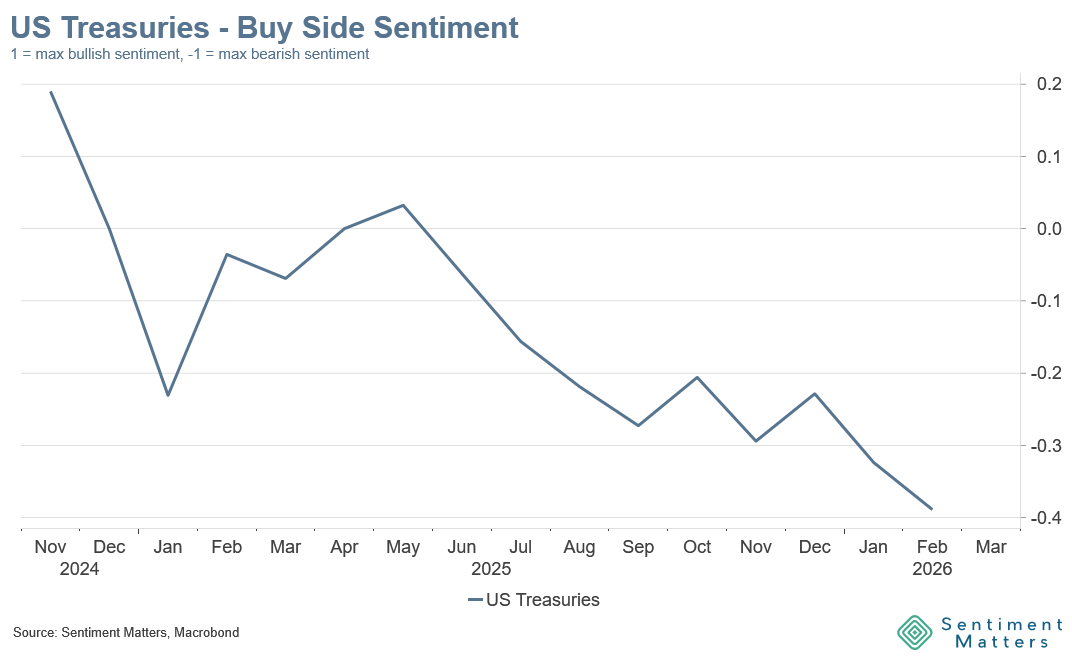

Net bearish: US Treasuries, Bunds, JGBs

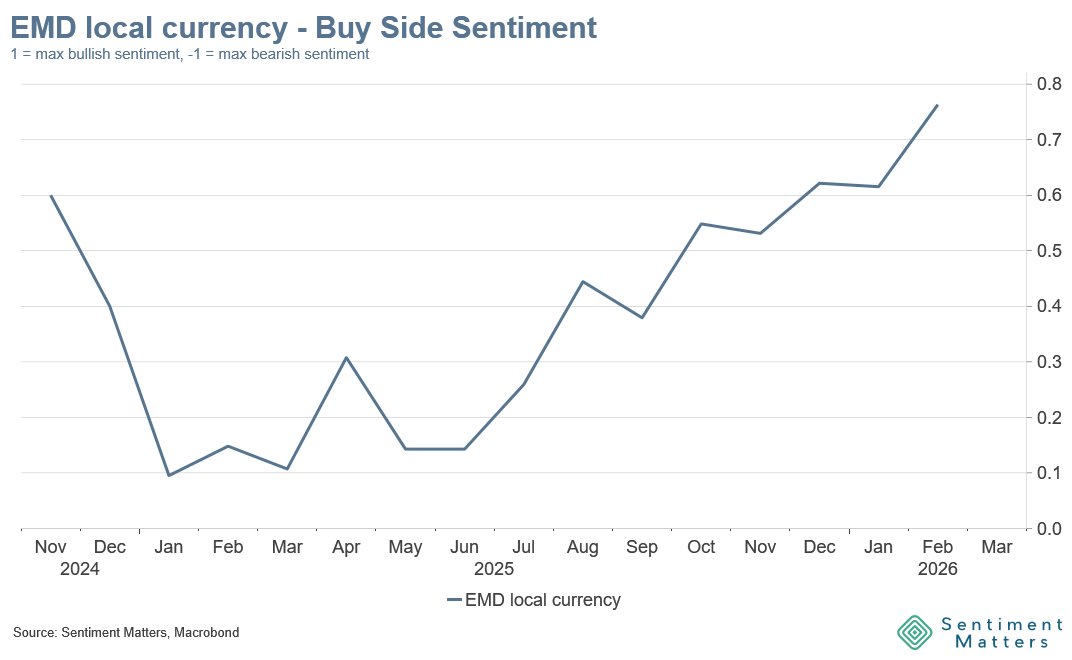

Net bullish: EMD, Gilts, Linkers

Highlights

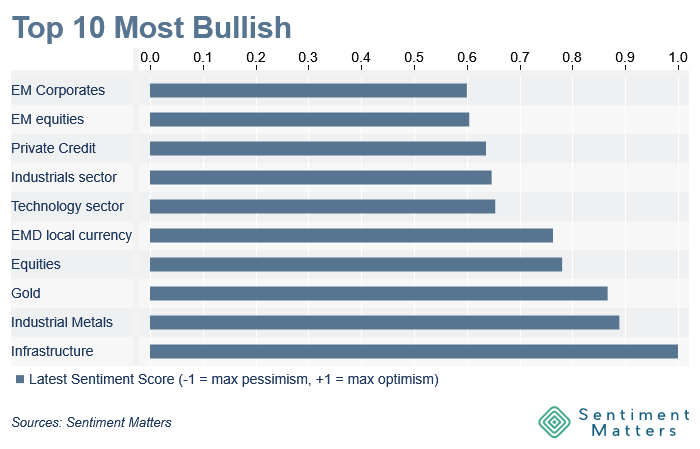

Local-currency EMD: #1 sovereign for the 5th straight month; upgraded again to +76% net bullish (BSST record). Now the 4th most popular asset in the tracker. Hard-currency EMD upgraded too, but the gap remains.

Gilts: downgraded, but still most popular DM sovereigns at +42% net bullish

JGBs: steady comeback as BOJ shifts and yields rise; bearishness easing back toward neutral

Bunds: upgraded from a low level, but still -16% net bearish

US Treasuries: another downgrade to a new tracker low at -39% net bearish — 4th least popular asset in the whole tracker

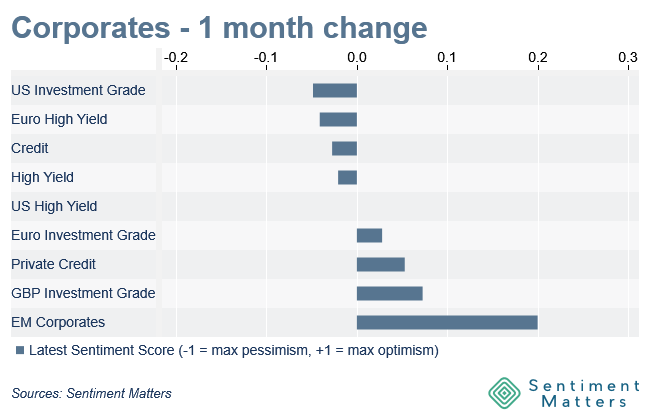

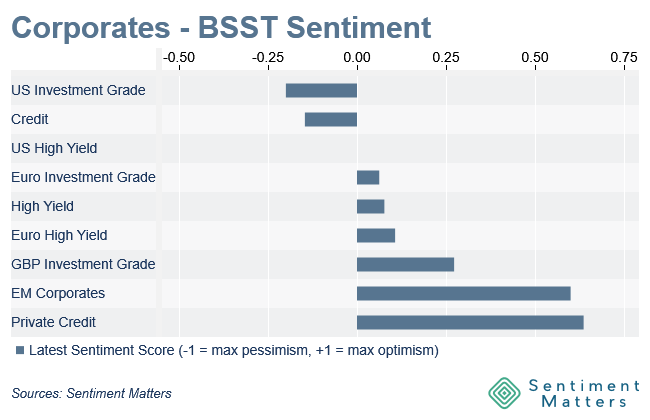

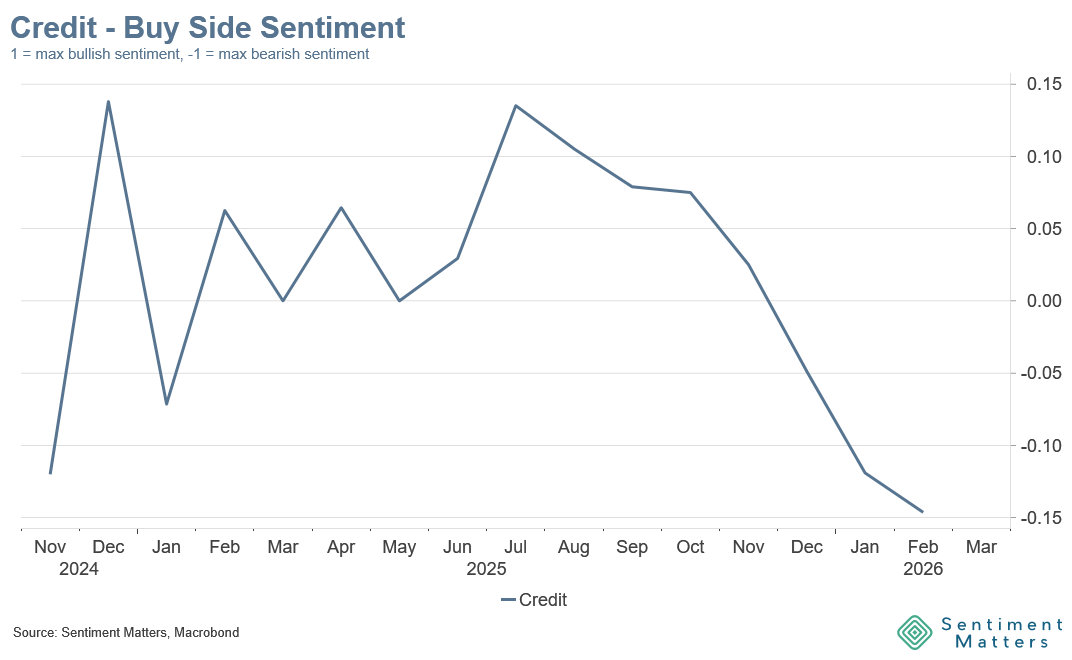

Credit

Private Credit: first upgrades since September. Still very popular at +64% net bullish, even if the extreme crowding of a year ago has faded. Sentiment is not yet low enough to offer much downside protection.

Investment Grade: small downgrades; 7th straight month of downgrades at the asset-class level. Preference remains Europe > US.

High Yield: small downgrade; still preferred to IG, again Europe > US.

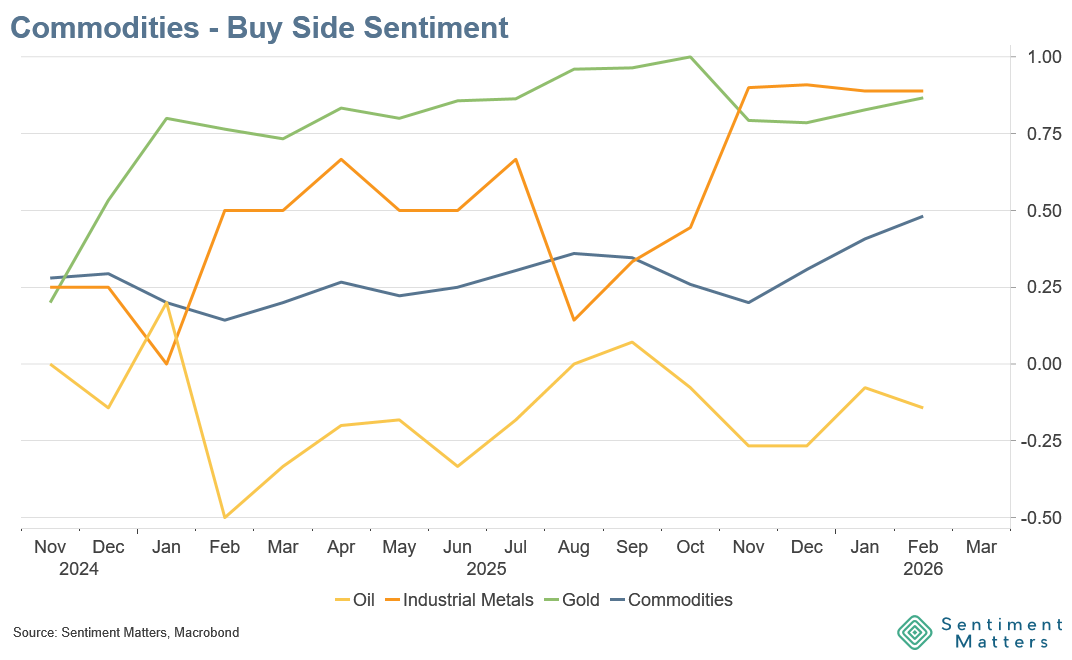

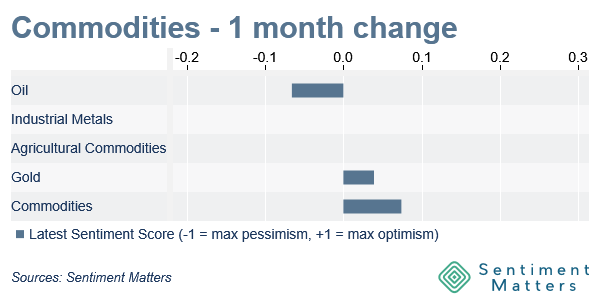

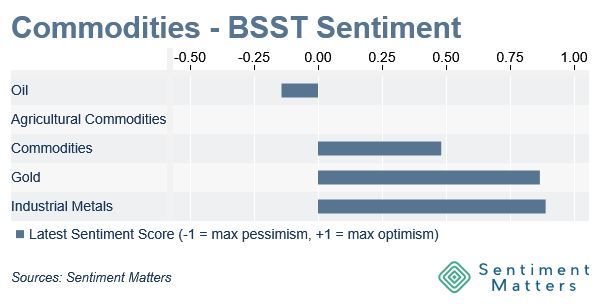

Commodities

Gold: second straight month of upgrades; +88% net bullish (2nd-most popular asset)

26 Bulls | 4 Neutrals | 0 Bears

Industrial metals: already near max bullish at +90% net bullish — almost everyone with a view is bullish

Oil: surprising downgrade given performance and Energy upgrades — leaves oil roughly neutral, consistent with other sentiment indicators

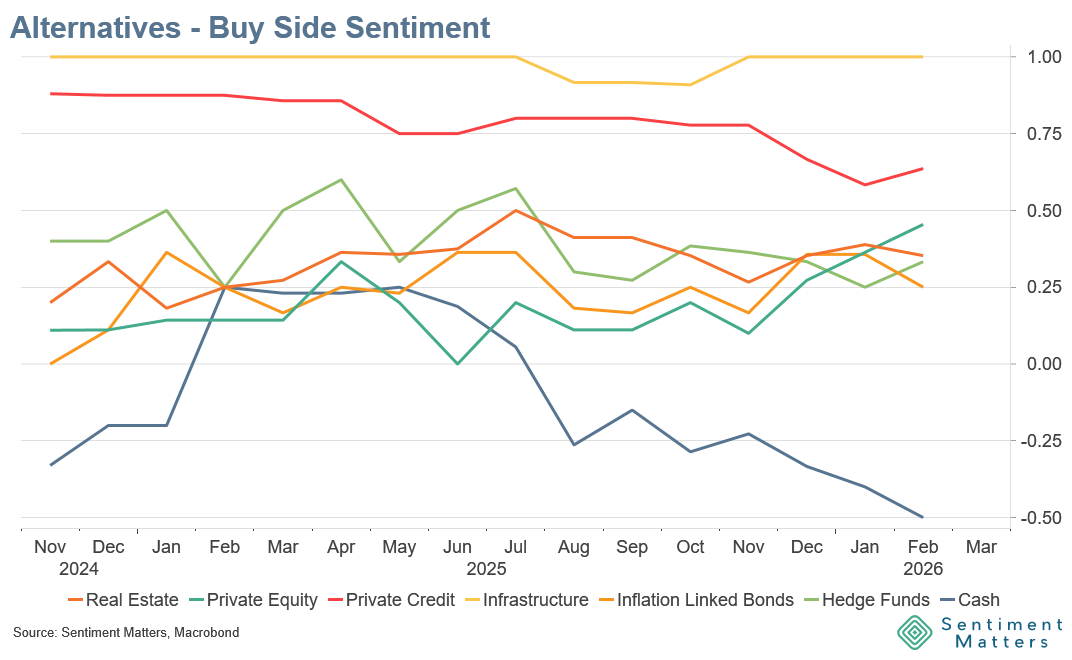

Alternatives

Infrastructure: universally loved — 100% bullish (16 Bulls, 0 Neutrals/Bears)

One-sided narratives can persist, but the vulnerability to negative news rises (we’ve seen this dynamic before in Gold and Private Credit).

Private rotation: Private Equity gaining fans as Private Credit loses them — looks like rotation within privates, not abandonment.

Have a great week — and good luck out there.

—Lars